The First 401(k)

- Bruce White

- Johnson, Kendall & Johnson

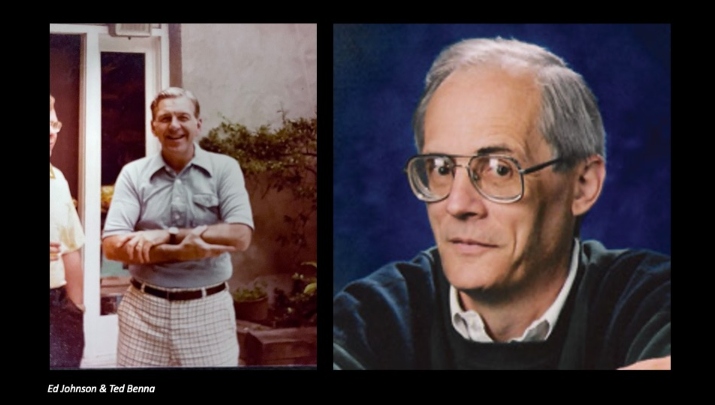

Today, the 401(k) is the standard for retirement savings in American companies of all sizes, industries, and ownership structures. Would it surprise you to learn that this has only been true for about 40 years? The very first 401(k) savings plan was created in 1980 by Ted Benna, an employee at the former parent company of Johnson, Kendall & Johnson (JKJ), the Johnson Companies. Benna’s pioneering plan was and remains one of the most important and wide-ranging People First developments across businesses nationwide.

In the 1980s, the Johnson Companies contained several divisions, the largest of which, Johnson Administrators, administered data for third parties on its considerable computer systems. A smaller division, Johnson Benna, did consulting on retirement plans. They mostly worked on non-qualified executive benefits plans for their clients, many of which were Fortune 500 companies.

More Articles and Videos

A Message in a Bottle: Tugboat Institute® Summit 2026

June 30, 2026

The History and Relevance of Juneteenth

June 16, 2026